“That Would Never Happen To Me” – Total Losses are More Common Than You Think

Why You Need Total Loss Shortfall Insurance

Many drivers assume accidents won’t happen to them or that comprehensive auto insurance covers everything. But the truth is that 34% if British drivers have written off a car, and when this happens, your car insurance company typically only pays out the current market value, not what you originally paid. This shortfall can leave you thousands of pounds out of pocket, making it difficult to replace your vehicle.

If you’ve never thought about what happens after a write off, this article will explore the possible shortfalls, the implications for your personal finance and the trusted solution from an award-winning insurance broker. It’s up to you to decide whether GAP insurance is worth it for your vehicle after learning the risks of driving without.

1 in 3 British Drivers Write Off a Car – Don’t Fall Short

Have you ever thought any of the following:

A write-off won’t happen to me

My comprehensive car insurance covers everything

I’ll cross that bridge when I come to it

It’s all too easy to avoid the initial cost of total loss protection. However, the problem with these sentiments is they leave you vulnerable to significant financial strain when the unexpected happens.

Statistics show that writing off a car is not as uncommon as most people think. Around 34% of UK drivers have written off a vehicle, with 7% experiencing this in the last five years alone. These numbers highlight just how real the risk is to everyday drivers. Yet, misconceptions about your auto insurance coverage often mean drivers are caught off guard.

Comprehensive motor insurance sounds reassuring, but it rarely provides the full safety net drivers assume it does. For example, if your vehicle is deemed a total loss after an accident, fire, or theft, your auto insurer will likely only cover the current market value of the car. This value depreciates rapidly, often up to 20% within months of owning a brand-new car. You could be out of pocket by thousands. Even pre-registered or used cars lose up to 40% of their value in the first three years.

Here’s where Guaranteed Asset Protection insurance changes the game. It protects you for up to 5 years, ensuring that, in the event of a write-off, we help you cover the shortfall between your motor insurer’s settlement and the cost of finding a replacement. While the specific insurance coverage for each GAP policy type varies, they’re designed to avoid a financial gap after a vehicle write-off.

We have a 99% GAP insurance payout rate for your peace of mind.

Not So Comprehensive Car Insurance

It’s surprising how many people misunderstand the limitations of comprehensive car insurance. Research shows that only 81% of UK drivers didn’t realise there was a financial shortfall after a write-off, without GAP coverage in place. 63% assumed that comprehensive auto insurance leaves no financial shortfalls.

These misconceptions can be devastating when faced with a total loss payout that doesn’t cover what you need to purchase a similar vehicle to the one you previously owned.

Secondly, it’s not uncommon to receive a market value settlement that falls short of what you deserve. GAP insurance companies try to negotiate the fairest settlement in case they try to underpay.

Comprehensive insurance often feels anything but ‘comprehensive’ when you’re forced to deal with a sudden financial shortfall. And it’s not just the depreciation you’ll have to cover. A total loss can leave you to pay outstanding auto loan, insurance excess or lease payments. That’s not even taking into account the price of a like-for-like model. The total shortfall can amount to thousands of pounds, which most drivers can’t readily afford

GAP insurance bridges this gap by covering the difference between your insurer’s payout and either the original price of your vehicle or the remaining loan balance. This means you’re able to replace your car without digging into savings, taking out loans, or settling for a lesser vehicle.

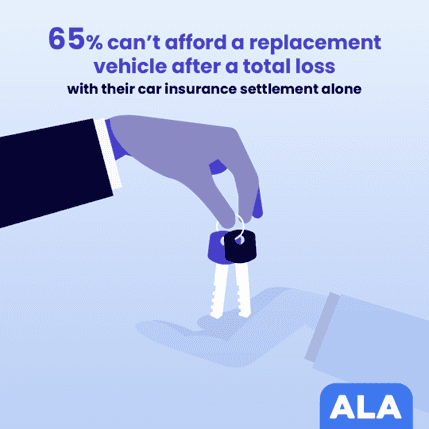

65% Can’t Afford a Replacement After a Vehicle Total Loss

It’s a sobering reality that two thirds of UK drivers couldn’t afford to replace their vehicle with their insurance payout alone; not even a market value alternative. This dire statistic not only highlights how comprehensive coverage can fail you after a total loss but emphasises a more pressing issue. You could face a financial disaster after a write-off.

When your car is written off, your insurer’s settlement will often cover the market value of the vehicle at the time of the accident or theft. However, the market value is usually significantly lower than what you originally paid, and replacing your car with a like-for-like model (similar to the one you bought) is often completely out of reach.

You could opt for a cheaper replacement but once you’ve paid off your loan balance or outstanding lease payments and other costs such as excess or negative equity, you’ll probably have to dig into your savings to find even a market value replacement anyway. Especially if your insurance payout is lower than you expected.

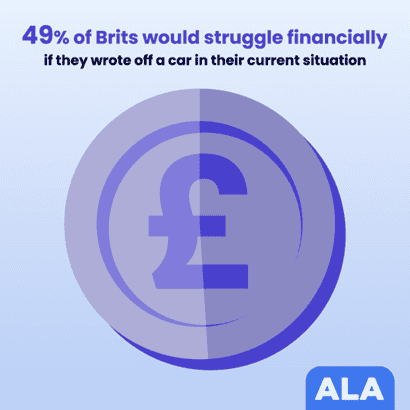

While half of Brits say they’d struggle financially if they wrote-off a car in their current situation, its not just about the financial gap. Finding the right replacement vehicle that suits your needs and budget can take time, especially since many of us are feeling the effects of the cost-of-living crisis. This could leave you and your family without a car or paying more than you budgeted for on a swift replacement or alternative travel arrangements.

This scenario is where GAP insurance proves valuable. By covering the financial gap, it ensures that you’re not left struggling to afford a replacement vehicle after a total loss. For many drivers, this peace of mind is invaluable.

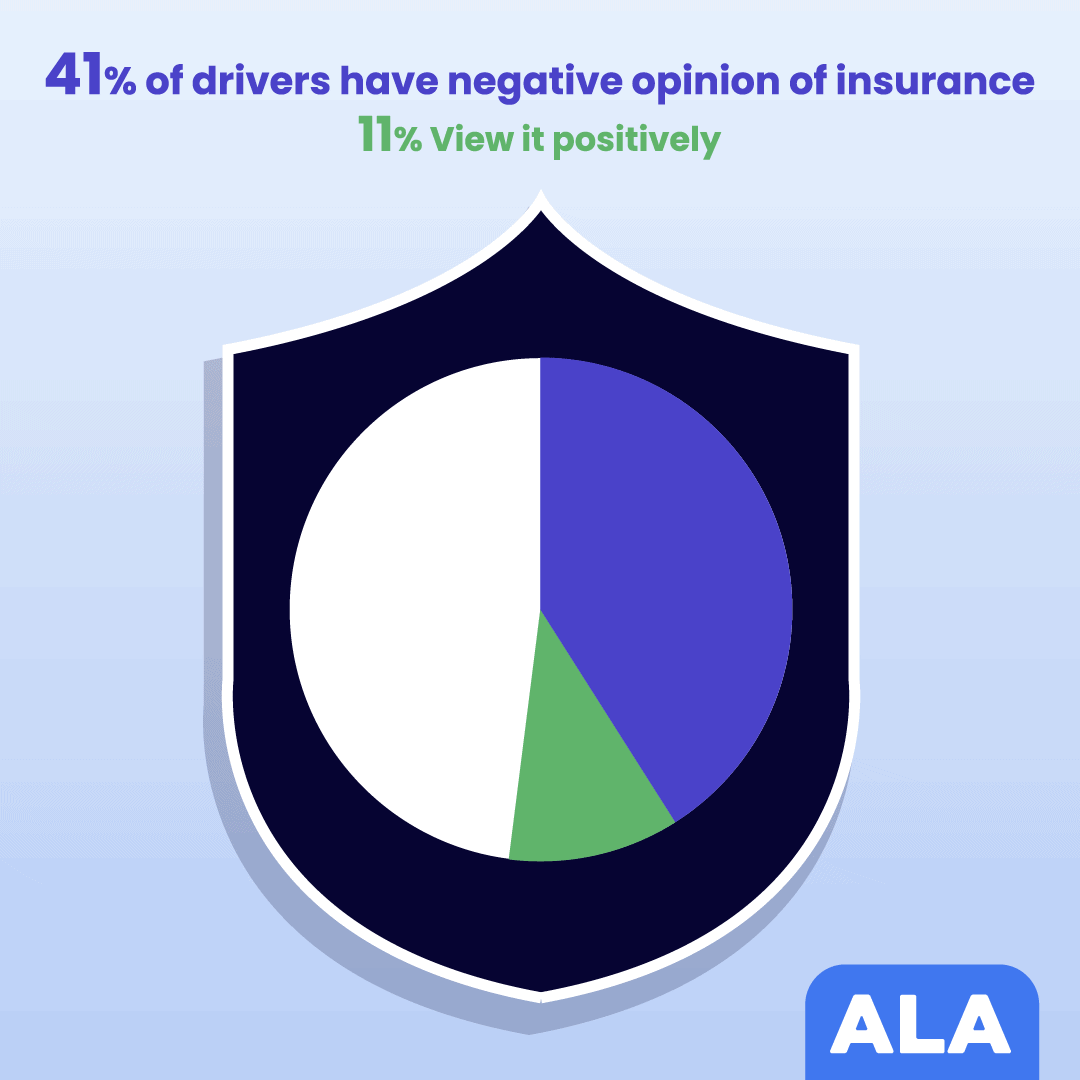

4x as Many Brits View Insurance Negatively vs Positively

It’s no secret that Brits have a poor view of insurance products. A recent survey revealed that 41% of drivers have a negative opinion of insurance, compared to just 11% who view it positively. This mistrust often stems from confusing policies, hidden fees, complex clauses and disappointing payouts, claims handling or customer service.

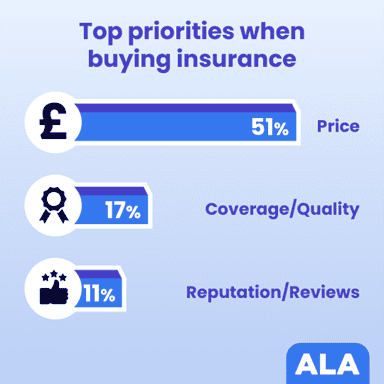

Despite this, only 11% of drivers prioritise reputation and reviews when shopping for an auto insurance policy, often putting a cheap price above all else (51%).

That’s why trust and transparency are key when choosing an insurer. ALA understands that drivers value straightforward, honest GAP coverage. With a 99% GAP insurance payout rate, no hidden fees, and award-winning customer service, ALA stands out as a trusted provider of GAP insurance coverage.

ALA’s GAP insurance policies are designed with drivers in mind. Explore the advantages:

Transparent:No hidden fees or surprise charges.

Flexible:Available for new and used cars, leased or purchased.

Inclusive:Covering cars from £5,000 to £125,000 in value. Read our full eligibility guide

Trusted:Backed by a 99% payout rate and outstanding customer reviews – we’re rated 4.9 stars on Trustpilot.

Competitive:We’re committed to giving our customers fair value and that means offering trusted policies at a competitive price.

Don’t fall victim to the assumption that “it won’t happen to me.” Writing off a car is more common than you think, and the financial consequences can be severe. With , you can drive confidently, knowing that you’re protected from a large financial gap.