Are you talking about the weather more than usual? Experts suggest that the UK is not prepared for extreme weather conditions likely to occur more frequently in the near future. Due to climate change, weather patterns are more unusual, leading to more aggressive storms, relentless wet weather, or scorching springs and summers.

Heavy rain, high winds, hail and flooding are particularly dangerous because they can cause a rail or car accident. Violent storms cause an average of £2,000 of damage yearly per British household, with the average flood damage bill standing at a staggering £30,000.

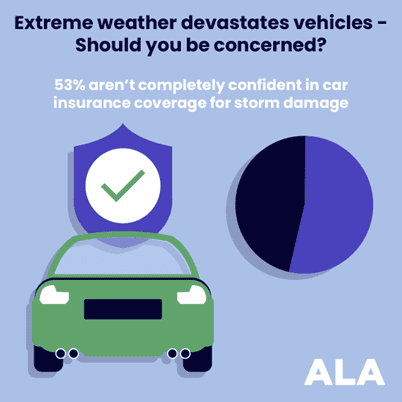

Third-party or collision coverage won’t protect against the repair cost and even a comprehensive car insurance policy has limits if your car is written off by storm damage. Should you worry about extreme weather causing vehicle damage?

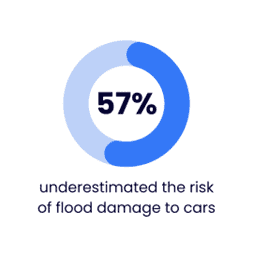

The UK never gets a shortage of downpours, nevertheless, the flood risks are increasing yearly and the country is not prepared for the extreme weather brought on by climate change. 1.9 million people live in areas at high risk for flooding, a number expected to double by 2050. The cost-of-living crisis puts an even greater strain on British households, making it even more devastating if the worst happens.

Flood damage is the number one risk factor for vehicle damage – 70% of flood-damaged cars are written off. According to the ABI (The Association of British Insurers), 20% of all vehicle write-offs (including collisions and thefts) are caused by bad weather conditions. Moreover, flooding and strong wind are the top two perpetrators of car damage.

Even if you avoid driving during a storm, your parked vehicle can still become a total loss. If you live in a high-risk area for floods, park on higher ground when there’s heavy rainfall and avoid parking near trees during a severe storm.

Without the right protection, severe weather could cost you! Less than 5% have total loss cover, so a flood or storm could put you in the red. Discover the money-saving power of GAP insurance!

Will your car insurance keep you afloat?

Although these are ‘at-fault claims’, so you lose your no-claims discount, comprehensive car insurance covers adverse weather damage. Your motor insurer pays the repair cost over your agreed excess or offers a market value settlement.

If you have third-party insurance or collision coverage, they won’t cover storm damage. It might be worth considering comprehensive coverage if you’re worried about bad weather damaging your car. Moreover, with a comprehensive insurance policy, you can add affordable GAP cover for complete peace of mind during a storm.

Over half of Brits don’t have full confidence in their car insurance company to cover storm damage – you might have third-party cover or worry about possible unforeseen costs. Despite the rising cost of premiums, a significant number are losing trust in their car insurance company. Aviva makes record profits despite losing thousands of customers. Meanwhile, Direct Line customers are warned by the FCA for undervaluing write-offs. Always investigate whether your auto insurance settlement is fair and find ways to save money on car insurance.

Should you worry about bad weather writing off your car?

Weather damage makes up a significant portion of vehicle write-offs. Stormy weather puts your vehicle at unnecessary risk of irreparable damage, particularly flooding. A costly repair claim or write-off could leave you in a financial predicament without proper insurance protection to future-proof your assets.

If you’re one of the 56% that worries about bad weather damaging their car, you’ll want to consider protecting yourself and your vehicle. Firstly, avoid driving during a storm and never drive through waterlogged roads. Even a small depth of water can cause your tyres to lose grip on the tarmac, risking an accident. Puddles on the road can be deceptively deep and water damage is the most common cause of a weather-related insurance claim.

While you wait out the bad weather, make sure to park your car on higher ground and away from trees. If you can, park close to buildings and avoid power lines. Ensure your windows and sunroofs are closed and use car covers or wax treatments to protect against scratches from flying debris.

Never drive through waterlogged or flooded roads

Avoid driving during a storm

Park uphill

Park away from trees and power lines

Close windows and sunroofs

Use car covers or wax treatments to protect the bodywork from debris

Use GAP insurance to protect against a total loss shortfall

What if your car is written off in a storm?

There’s not much you can do once your vehicle is declared a total loss. Your insurer decides whether your repair is either possible or economical; if it’s neither, they’ll write the car off. However, with GAP insurance, you protect yourself from the significant shortfall you may incur with buying your next vehicle. We top up your car insurance settlement to help you afford a replacement vehicle after a total loss.

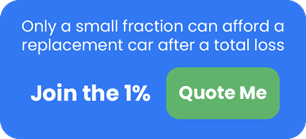

Only 17% of Brits can afford even a like-for-like replacement vehicle with their insurance settlement after a total loss, so GAP insurance is a good idea to help you afford a new car if the unexpected occurs.

Guaranteed Asset protection tops up your total loss settlement to cover vehicle depreciation, outstanding car finance, lease payments, deposits, and other total loss shortfalls you may encounter. Don’t be left out of pocket if your car’s written off this winter.

There are four types of GAP insurance, Back to Invoice, Vehicle Replacement, Contract Hire and Agreed Value. Together, they cover almost any vehicle, regardless of how or where you bought it. There are also no age and mileage limits for Agreed Value policies, making GAP coverage even more accessible. A GAP insurance policy can last three to five years and cost as little as a standard gym membership, paid over just ten months.