Are you trying to choose the right cycling insurance for your cycling needs? We compare ALA Cycle Insurance to a well-known insurer – Direct Line. We compare the standard coverage between the two policies, the price for a standard insurance policy and one matched for coverage. We discuss excess options, the top benefits of each policy, and why you may want to choose it.

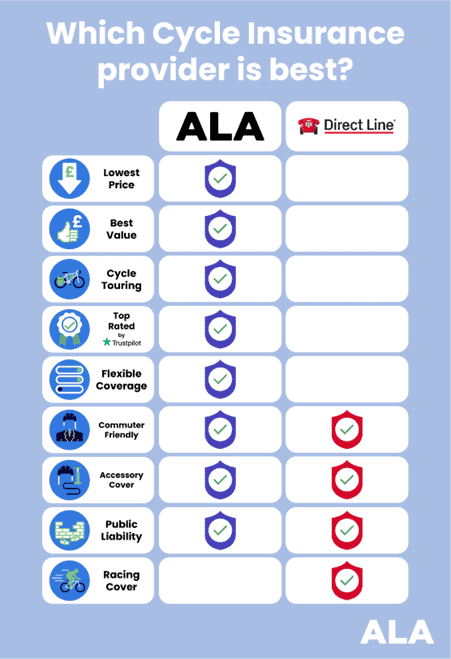

As standard, ALA covers malicious and accidental damage, bicycle theft and travel insurance for your bike for up to 30 days. We have fully customisable plans to suit your cycling needs. If you need more coverage, you can add the following options and even select your necessary cover limits.

Bike accessory cover up to £300 or £900

Replacement bike hire cover up to £500 or £1,000

Public liability insurance up to £1m or £2m

Legal expenses up to £25,000

Personal accident cover up to either £10,000 or £25,000

What does Direct Line bike insurance cover?

Direct Line covers malicious and accidental bicycle damage, public liability and accessory cover up to £250 as standard. You can also add cycling travel insurance, cycling race cover and personal accident cover for additional insurance premium.

Both policies require policyholders to take adequate care of their bicycles, including storing them in a secure, private location or with an approved lock by Sold Secure that matches the bicycle’s value.

Which insurance cover is the most affordable?

The policies offer slightly different coverage. However, ALA comes out on top for affordability. When matched for insurance excess, standard ALA Insurance (2023) for a £1,000 bike costs £62.32 per year. Meanwhile, a policy with Direct Line for the same bicycle value is £125.

Bicycle theft, damage, travel Public Liability (cover limit not stated) and accessory cover up to £250.

£132

Which insurance has the lower excess?

Direct Line offers a flat rate excess, meaning every insurance policy will have a £50 excess. Although this means you have less to pay when you make a claim, it also means you cannot increase your excess to reduce your premium. ALA allows you to choose between three excess options: £50, £150, and £250.

You want to choose an insurance policy excess that is around 10% of the value of your bike so that both your premium and potential excess are affordable for you.

Direct Line don’t allow you to choose your excess, making their policies less flexible. On the other hand, Direct Line can cover lost race fees if you’re a professional cyclist.

Unfortunately, ALA can’t cover professional bicycle use, including racing, courier cycling or other commercial use. However, overall, our policies are more customisable.

Which bike insurance should I choose?

The bottom line is you should choose the insurance policy coverage that suits your cycling activities and your budget; we outline the benefits of each policy below:

Cover restrictions vary from provider to provider, but insurers generally can’t cover bikes stored against security requirements. Insurers can’t always cover bikes used for hire and reward purposes. Age restrictions may also apply. Learn about the limitations of Cycle Insurance.

How expensive is specialist Cycle Insurance?

Specialist Cycle Insurance allows you to build a policy to suit your unique needs and budget. Higher levels of coverage will cost more. However, some providers are more cost-effective than others. ALA offers better value than Direct Line overall and when matched for coverage options, bike value and excess.

What is a good excess for cycle insurance?

The cycle insurance excess is a pre-agreed amount you pay when making a claim. Usually, the higher the excess, the lower the premium and vice versa. You should set your excess to an amount you can afford to pay should you need to claim. You can increase your excess to reduce your premium. A general rule of thumb is to select an excess amount that is approximately 10% of the cost of your bike.

{kind=link}